Mortgage Experience you can rely on

Trust us to help you find the right mortgage options and products for your current financial situation.

Mortgage financing can be confusing, it doesn't have to be, here's the plan.

Get started right away

The best place to start is to connect with us directly. The mortgage process is personal. Our commitment is to listen to all your needs, assess your financial situation, and provide you with a clear plan forward.

Get a clear plan

Sorting through all the different mortgage lenders, rates, terms, and features can be overwhelming. Let us cut through the noise, we'll outline the best mortgage products available, with your needs in mind.

Let us handle the details

When it comes time to arranging your mortgage, we have the experience to bring it together. We'll make sure you know exactly where you stand at all times. No surprises. We've got you covered.

Let's run some numbers.

Start by telling us where you're at in your home buying journey.

Check Out Our Team

What people that work with us are saying

Home Buyers Tips

Everything you need, all in one place.

We can help you arrange mortgage financing for these services:

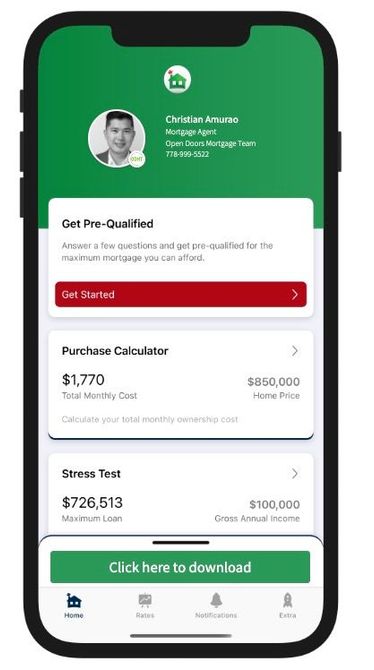

DOWNLOAD MY MORTGAGE TOOLBOX

WHAT YOU CAN DO WITH MY APP:

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese

LET'S RUN SOME NUMBERS

The Calculator Hub

Purchase Calculator

Calculate your total monthly cost and the minimum required down payment.

Closing Costs

Calculate closing costs including transfer taxes, first-time buyer rebates, new home rebates and ancillary costs.

Compare side by side

Compare up to four scenarios side by side to see which option is best for you.

Mortgage Calculator

Easy to use Canadian Mortgage Calculator jam-packed with awesome features.

Maximum Mortgage

Calculate the Maximum Mortgage you can afford with an affordability slider.

Required Income

Estimate how much annual income you need for any size mortgage.

Property Transfer Tax

Calculate your property transfer taxes including first-time home buyers and the newly built home rebates.

Renewal Calculator

Find out how much your payments will increase or decrease at renewal time.

Debt Service Calculator

Calculate debt service ratios with an incredible level of accuracy.

OUR BLOG IS KEPT UP TO DATE SO YOU CAN STAY INFORMED!

The idea of owning a vacation home—your own cozy escape from everyday life—is a dream many Canadians share. Whether it’s a lakeside cabin, a ski chalet, or a beachside bungalow, a second property can add lifestyle value, rental income, and long-term wealth. But before you jump into vacation home ownership, it’s important to think through the details—both financial and practical. Start With Your 5- and 10-Year Plan Before you get swept away by the perfect view or your dream destination, take a step back and ask yourself: Will you use it enough to justify the cost? Are there other financial goals that take priority right now? What’s the opportunity cost of tying up your money in a second home? Owning a vacation home can be incredibly rewarding, but it should fit comfortably within your long-term financial goals—not compete with them. Financing a Vacation Property: What to Consider If you don’t plan to pay cash, then financing your vacation home will be your next major step. Mortgage rules for second properties are more complex than those for your primary residence, so here’s what to think about: 1. Do You Have Enough for a Down Payment? Depending on the type of property and how you plan to use it, down payment requirements typically range from 5% to 20%+ . Factors like whether the property is winterized, the purchase price, and its location all come into play. 2. Can You Afford the Additional Debt? Lenders will calculate your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios to assess whether you can take on a second mortgage. GDS: Should not exceed 39% of your income TDS: Should not exceed 44% If you’re not sure how to calculate these, that’s where I can help! 3. Is the Property Mortgage-Eligible? Remote or non-winterized properties, or those located outside of Canada, may not qualify for traditional mortgage financing. In these cases, we may need to look at creative lending solutions . 4. Owner-Occupied or Investment Property? Whether you’ll live in the home occasionally, rent it out, or use it strictly as an investment affects what type of financing you’ll need and what your tax implications might be. Location, Location… Logistics Choosing the right vacation property is more than just finding a beautiful setting. Consider: Current and future development in the area Available municipal services (sewer, water, road maintenance) Transportation access – how easy is it to get to your vacation home in all seasons? Resale value and long-term potential Seasonal access or weather challenges What Happens When You’re Not There? Unless you plan to live there full-time, you'll need to consider: Will you rent it out for extra income? Will you hire a property manager or rely on family/friends? What’s required to maintain valid home insurance while it’s vacant? Planning ahead will protect your investment and give you peace of mind while you’re away. Not Sure Where to Start? I’ve Got You Covered. Buying a vacation home is exciting—but it can also be complicated. As a mortgage broker, I can help you: Understand your financial readiness Calculate your GDS/TDS ratios Review down payment and lending requirements Explore creative solutions like second mortgages , reverse mortgages , or alternative lenders Whether you’re just starting to dream or ready to take action, let’s build a plan that gets you one step closer to your ideal getaway. Reach out today—it would be a pleasure to work with you.

In recent years, housing affordability has become a significant concern for many Canadians, particularly for first-time homebuyers facing soaring prices and strict mortgage qualification criteria. To address these challenges, the Canadian government has introduced several housing affordability measures. In this blog post, we'll examine these measures and their potential implications for homebuyers. Increased Home Buyer's Plan (HBP) Withdrawal Limit Effective April 16, the Home Buyer's Plan (HBP) withdrawal limit will be raised from $35,000 to $60,000. The HBP allows first-time homebuyers to withdraw funds from their Registered Retirement Savings Plan (RRSP) to use towards a down payment on a home. By increasing the withdrawal limit, the government aims to provide young Canadians with more flexibility in saving for their down payments, recognizing the growing challenges of entering the housing market. Extended Repayment Period for HBP Withdrawals In addition to increasing the withdrawal limit, the government has extended the repayment period for HBP withdrawals. Individuals who made withdrawals between January 1, 2022, and December 31, 2025, will now have five years instead of two to begin repayment. This extension provides borrowers with more time to manage their finances and repay the withdrawn amounts, alleviating some of the immediate financial pressures associated with using RRSP funds for a down payment. 30-Year Mortgage Amortizations for Newly Built Homes Starting August 1, 2024, first-time homebuyers purchasing newly built homes will be eligible for 30-year mortgage amortizations. This change extends the maximum mortgage repayment period from 25 years to 30 years, resulting in lower monthly mortgage payments. By offering longer amortization periods, the government aims to increase affordability and assist homebuyers in managing their housing expenses more effectively. Changes to the Canadian Mortgage Charter The government has also introduced changes to the Canadian Mortgage Charter to provide relief to homeowners facing financial challenges. These changes include early mortgage renewal notifications and permanent amortization relief for eligible homeowners. By implementing these measures, the government seeks to support homeowners in maintaining affordable mortgage payments and mitigating the risk of default during times of financial hardship. The recent housing affordability measures announced by the Canadian government are aimed at addressing the challenges faced by homebuyers in today's market. These measures include increasing withdrawal limits, extending repayment periods, and offering longer mortgage amortizations. The goal is to make homeownership more accessible and affordable for Canadians across the country. As these measures come into effect, it's crucial for homebuyers to stay informed about the changes and their implications. Consulting with a mortgage professional can help individuals explore their options and make informed decisions about their housing finances. If you're interested in learning more about these changes and how they may affect you, please don't hesitate to connect with us. We're here to walk you through the process and help you consider all your options and find the one that makes the most sense for you.

If you’re a homeowner looking to optimize your finances, consider taking advantage of your home’s equity to reposition any existing debts you may have. If you’ve accumulated consumer debt, the payments required to service these debts can make it difficult to manage your daily finances. A consolidation mortgage might be a great option for you! Simply put, debt repositioning or debt consolidation is when you combine your consumer debt with a mortgage secured to your home. To make this happen, you’ll borrow against your home’s equity. This can mean refinancing an existing mortgage, securing a home equity line of credit, or taking out a second mortgage. Each mortgage option has its advantages which are best outlined in discussion with an independent mortgage professional. Some of the types of debts that you can consolidate are: Credit Card Unsecured Line of Credit Car Loan Student Loans Personal or Payday Loans Most unsecured debt carries a high interest rate because the lender doesn't have any collateral to fall back on should you default on the loan. However, as a mortgage is secured to your home, the lender has collateral and can provide you with lower rates and more favourable terms. Debt consolidation makes sense because it allows you to take high-interest unsecured debts and reposition them into a single low payment. So, when considering the best mortgage for you, getting a low rate is important, but it’s not everything. Your goal should be to lower your overall cost of borrowing. A mortgage that allows for flexibility in prepayments helps with this. It’s not uncommon to find a mortgage at a great rate that allows you to increase your payments by 15% per payment, double your payments, or make a lump sum payment of up to 15% annually. As additional payments go directly to the principal repayment of the loan, once you’ve consolidated all your debts into a single payment, it’s smart to take advantage of your prepayment privileges by paying more than just your minimum required mortgage payment, as this will help you become debt-free sooner. While there is a lot to unpack here, if you’d like to discuss what using a mortgage to reposition your debts could look like for you, here’s a simple plan we can follow: First, we’ll assess your existing debt to income ratio. We’ll establish your home’s equity. We’ll consider all your mortgage options. Lastly, we’ll reposition your debts to help optimize your finances. If this sounds like the plan for you, the best place to start is to connect directly. It would be a pleasure to work with you.